I am indebted to my friends at 7IM for what follows.

During these very uncertain times, all fund managers and financial advisers have received many questions about the economy and prospects for investment returns going forward. 7IM have collected those most frequently asked and offer their insights below.

By the way, the question I personally have been asked more than any other recently is number 5. The answer provided by 7IM is verbatim my usual response, as clients who have asked me this question will attest.

1. Why has the significant fall in oil and gas prices not yet fed through to much lower inflation levels?

Ahmer Tirmizi, Head of Fixed Income Strategy

Inflation is defined in different ways. For some, it’s just a number, defined as the growth in prices - an objective measure without debate. For others, inflation is something that is felt - we remember how much the weekly shop costs us compared to last time. Particularly when everything is going up.

Take petrol prices. We find it easy to remember that petrol prices had at one point doubled from the lows of the Covid recession to the highs of 2022. Every time we go to the pumps, we remember that feeling of filling up at or above £2 per litre. At the same time, food prices were going up, housing costs were going up… every cost was going up. Rising petrol was just another squeeze on incomes. However, on the flipside, we don’t feel that much happier now that petrol prices are down by a quarter from their 2022 highs; or that they are below the level they were when Russia invaded Ukraine. What’s even harder to believe is that, as they stand right now, petrol prices aren’t that different to what they were 10 years ago. Prices have gone from around £1.35/litre to £1.45/litre in that time - that’s around 0.7% rise per year.

So, it turns out the fall in oil prices has led to falls in the cost of filling up. However, while it might be in the numbers, until other prices fall more widely, we are unlikely to feel it. Going forward, we believe the overall inflation basket is close to peaking and will start to fall soon. The last inflation print in the UK shows inflation falling substantially from its peak. It will be a slow and bumpy process, but eventually, we will start to see and feel inflation coming down to more normal levels.

2. Are we facing a banking crisis similar to 2008?

Salim Jaffar, Investment Analyst

In one word. No.

The global financial crisis was many years and mistakes in the making. Risky lending practices that were facilitated by decades of deregulation ultimately led to an extreme housing bubble and its eventual bursting. This led to the collapse of a number of major financial institutions. Unfortunately, almost everyone was impacted since most people have some financial tie to housing… as Edward Leamer said, “housing is the business cycle”.

What’s going on at the moment is different.

In the US, some non-systemically important banks have mismanaged their balance sheet risk. Rising rates meant that the bonds they held as collateral against deposits couldn’t be sold for enough when people tried to redeem their deposits.

In Europe, something largely unrelated happened. For years Credit Suisse had been struggling with reputational issues as a result of being pretty near the centre of the majority of banking scandals over the past few years. On top of this, the bank was having serious profitability issues. This is what allowed for the speed and scale of deposit flight that we saw. Currently, no other systemically important European or US banks are finding themselves in this kind of hot water.

The 2008 crisis was economy-wide. What’s going on right now with banks is not economy-wide.

3. Should we be worried about the US debt ceiling?

Ben Kumar, Head of Equity Strategy

The debt ceiling is not an economic problem – the US can borrow money, and will pay it back – it’s a political one, created by the strange and complex system that is US politics.

We’ve had a century of shenanigans with the debt ceiling (it was introduced in 1917). Each time, a solution is found, that makes the whole thing even more roundabout and complicated to resolve next time, but ultimately sorts it all out.

The solution this time will be tense and nerve-racking if you follow the minutiae of Congressional activity. But if you can ignore the breathless reports from Washington DC, the world will keep on turning – soon we’ll be needlessly worrying about the 2024 election instead. Sigh.

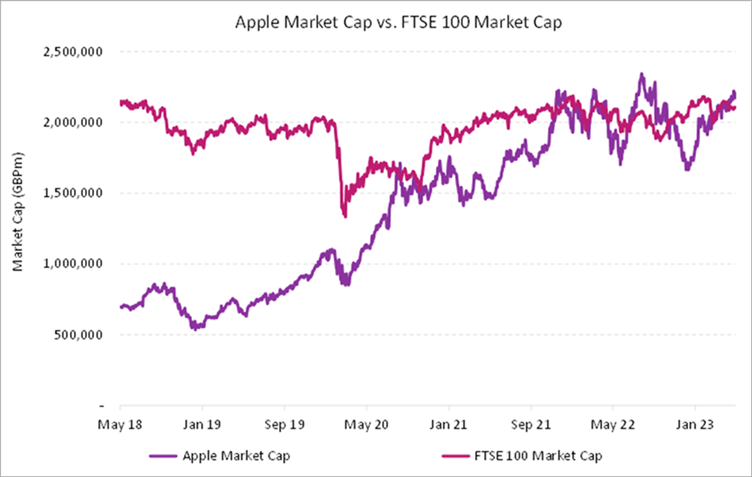

4. The UK economy seems to be more resilient than expected. Does this mean it’s an opportune place to invest?

Salim Jaffar

It can be argued that the UK has been surprisingly resilient, but I think there are two main points to unpick here:

Investing in the FTSE 100 isn’t really investing in the UK economy, it’s just investing in companies that are historically listed in the UK. Less than 20% of the revenue earned by FTSE 100 companies comes from the UK. This is one reason why the UK market has been quite resilient despite high inflation and other economic indicators suggesting that the UK is struggling.

A second point I would make is that the main reason the FTSE 100 has performed well over the past couple of years is mostly because of the sectors that make up the index. The FTSE 100 is concentrated in sectors such as financials, healthcare, and energy, which have stood up well to post covid challenges in a way other sectors haven’t.

This is why we think that there are opportunities in the UK; you just have to be a little more selective than holding all UK-listed companies, which is why we hold the FTSE 100 as opposed to the FTSE All-share or 250, and also why we have specific sector allocations to healthcare, materials, and bank debt.

5. In a world of higher interest rates, is investing still worth it? Surely cash is now more attractive?

Ben Kumar

Let’s address the big point. Cash rates on bank accounts are more attractive than they’ve been in a long time. But inflation is far worse than it’s been in a long time too…

So, while it was grim getting paid 0% on savings through the 2010s, it helped that inflation was around 2%. Your cash was worth about 2% less by the end of every year. Now, although you might get 3% or 4% on a bank account, inflation is at 9%! You’ll get some interest, which is nice – but even after that, your cash is worth ~5% less by the end of the year!

Until savings rates are above inflation, cash is a negative return strategy – guaranteed.

Whereas investing isn’t a guaranteed return (have you read all of the disclaimers!?), it is one which, over time, can help to beat inflation. In fact, investing in the shares of a company is a way to get inflation working for you rather than against you. Those price increases which make our shopping more expensive are being made by the very companies you invest in! Company earnings tend to beat inflation over time as the management teams increase prices and cut costs. That’s better than the bank manager is doing on your savings account!

6. Why do you think there’s likely to be a recession in the US? How bad, and what are the risks?

Ahmer Tirmizi

Recessions are often thought of as events, and we label them as such. The Lehman Brothers default of 2008 or the Y2K bust of the early 2000s. In truth, they’re not usually specific events with specific dates but rather processes. These processes involve a messy interaction between businesses, consumers and governments that leads to the economy slowing down, so much so that it eventually contracts.

While each recession is labelled differently, the process often follows a very similar pattern. Primarily, interest rates tend to rise sharply – if mortgage costs go up, households think twice about their next purchases. Additionally, prices (particularly necessities like food and energy) tend to rise sharply, squeezing incomes. This leads people to tighten their belts as they focus on the things they need (to heat their homes and feed their families) over the things they don’t (a new car or a holiday abroad). And finally, company profits tend to fall as spending comes down. If people buy less stuff, companies earn less money. And when profits fall, companies tighten their belts, potentially laying off workers as a result.

As things stand, these patterns are present today. We’ve seen the sharpest rises in interest rates in a generation. And we’ve also seen the sharpest rise in prices in a generation (even if they might be easing now). The impact is clear, consumers are slowly reining in their spending. Housing is slowing down and global manufacturing is contracting. Consequently profits, as measured by earnings per share, are down from the highs, with possibly more to come. These factors leave us positioned cautiously.

It isn’t all doom, though. Just like recessions, recoveries aren’t events with specific dates. They are processes with very similar patterns to the past. So, while those patterns are currently pointing to a recession, this won’t be forever. Eventually, our view is that interest rates and inflation will come down. And when they do, this will set in motion the subsequent economic recovery that will eventually take place.

7. Are there any opportunities to MAKE money in a recession?

Ben Kumar

Of course! You just have to be patient and prepared to hold your nerve.

Some investments, such as healthcare companies, should do well because their earnings stream isn’t related to the economic cycle – other investors will rotate out of their cyclical exposures into healthcare.

Other investments, such as mining companies, should do well because they’re already cheap – a recession can’t really hurt them much more, and they’re paying out a nice chunky dividend yield.

And, investing in government bonds in a recession has tended to work. Rates fall, bond prices rise. US treasuries and UK Gilts aren’t exciting. But they work!

Graham’s Summary

Pulling all of those questions and answers together, we end up once again with the view that, whatever the turbulence we are currently facing, the principles of disciplined long-term investing have not changed. These issues will pass and markets will progress once again …….. as they ALWAYS have in the past.

I hope you have found this interesting but, if you have any questions about this piece or any other finance related matter, please do not hesitate to get in touch.

Yours sincerely,