You will doubtless be aware of the problems faced by ‘Star’ investment manager Neil Woodford over the past couple of weeks and I have been meaning to write one of my blogs on the subject; well my good friend from Northern Ireland, David Crozier, has beaten me to it and I am sure he won’t mind me sharing his piece with you.

“Spare a thought for anyone invested in the Woodford Equity Income Fund, managed by Neil Woodford. The fund was suspended this week, following an unexpectedly high level of clients taking their money away from the fund. When Kent County Council wanted to withdraw the £263 million they had invested, Mr Woodford suspended trading in the fund, to protect all of the investors in the fund, which means that no-one can get their money out.

The Woodford Fund invests in some unquoted companies, which cannot be easily sold, and does so in a much a higher proportion than most other funds. When investors lose confidence and start to sell, these illiquid investments can’t be sold quickly or easily, and therefore to pay out the redemptions, mainstream, liquid, lower risk companies have to be sold. This means that the proportion of risky, illiquid stocks rises – it was up to 18% of the fund at one point.

There is absolutely no doubt that Neil Woodford has in the past delivered returns to investors in excess of what they could have obtained from simply investing in the market.

The question is, At what cost?

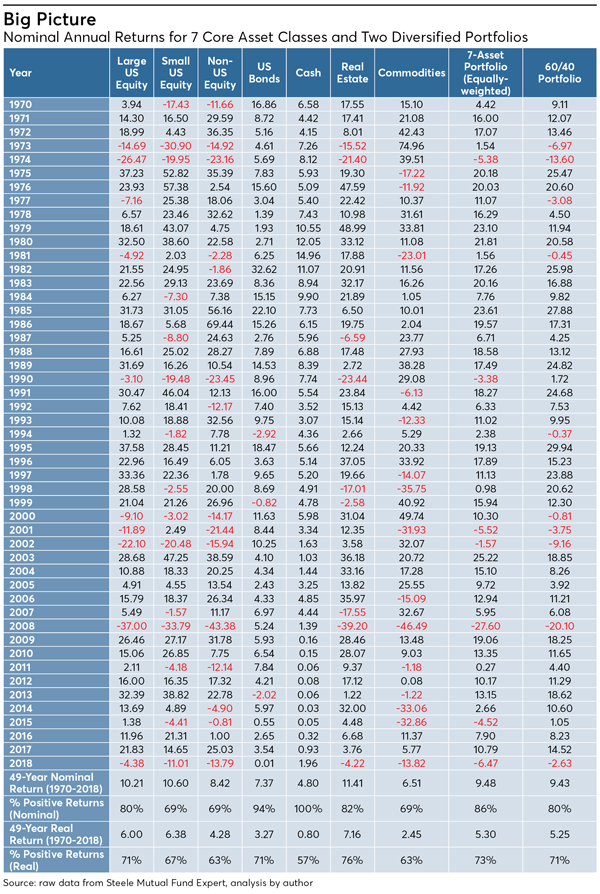

It is an immutable law of the universe that risk and reward are related, at least when it comes to investments. Attempting to achieve higher returns inevitably involves taking extra risk; it follows that taking extra risk should, in itself, lead to a higher return – the technical term for this extra return is called beta (β).

The difficult bit is achieving returns that are better than are due to investors simply for turning up and taking risk. The technical name for this excess return is alpha (α) and the evidence is that on average, over time, and after costs, α is very elusive.

The question is, has Mr Woodford consistently generated excess risk-adjusted return, alpha, through skill, or was there an element of luck?

If we could be reasonably sure that a particular investment manager’s outperformance is due to skill rather than luck it would make sense to use that manager, however this is also incredibly difficult to recognise. There is a mathematical reason for this; it’s all to do with statistics.

Suppose we have a fund that has experienced annual returns of 5%, and volatility of 20%. How long do you think it will take until there are enough data points to give any confidence that the results are due to skill rather than luck? A year? Two? Five?

How about 65 years!

Nobody, but nobody, has a track record that long, which is why it is very unwise to use a manager’s track record to judge whether he will be any good in the future.

Oh, and in case you are concerned about it, none of our client portfolios are invested in any Neil Woodford fund (or indeed any actively managed fund.)”

Like David’s firm in Northern Ireland, none of the Clearwater Portfolios have any exposure to Neil Woodford funds or any other actively managed fund, where the manager may be tempted to take greater risks in pursuit of elusive alpha!

If you have any concerns or questions about any finance related matter, please do not hesitate to call me at any time.

With best wishes,

Yours sincerely

Graham Ponting CFP Chartered MCSI

Managing Partner